Estimates the multifractal scaling properties of a time series using

the detrending moving average algorithm (Gu & Zhou 2010). Clean-room

C++ reimplementation from the published algorithm (the reference

MATLAB implementation consulted, MFDMA_1D.m, had no license header;

see inst/COPYRIGHTS). The segment-fluctuation core was validated

against a Python transliteration of that reference on synthetic test

data (exact match to displayed precision).

Usage

mfdma(

x,

n_min = 10L,

n_max = NULL,

n_scales = 30L,

theta = 0,

q = seq(-4, 4, by = 0.1)

)Arguments

- x

Numeric vector. The time series to analyse.

- n_min, n_max

Integer. Lower/upper bound of the segment size

n. Following the reference implementation's guidance:n_minaround10;n_maxaround 10% oflength(x). Defaults:n_min = 10,n_max = round(length(x) / 10).- n_scales

Integer. Number of segment sizes to evaluate (log-spaced between

n_minandn_max). Default30.- theta

Numeric in

[0, 1]. Position of the moving-average window:0(default, recommended) = backward MFDMA,0.5= centered,1= forward.- q

Numeric vector. Multifractal orders to evaluate. Default

seq(-4, 4, by = 0.1).

Value

A list with:

- n

Segment sizes evaluated.

- Fq

Matrix of the q-th order fluctuation function (segment size x q).

- tau

Multifractal scaling exponent tau(q).

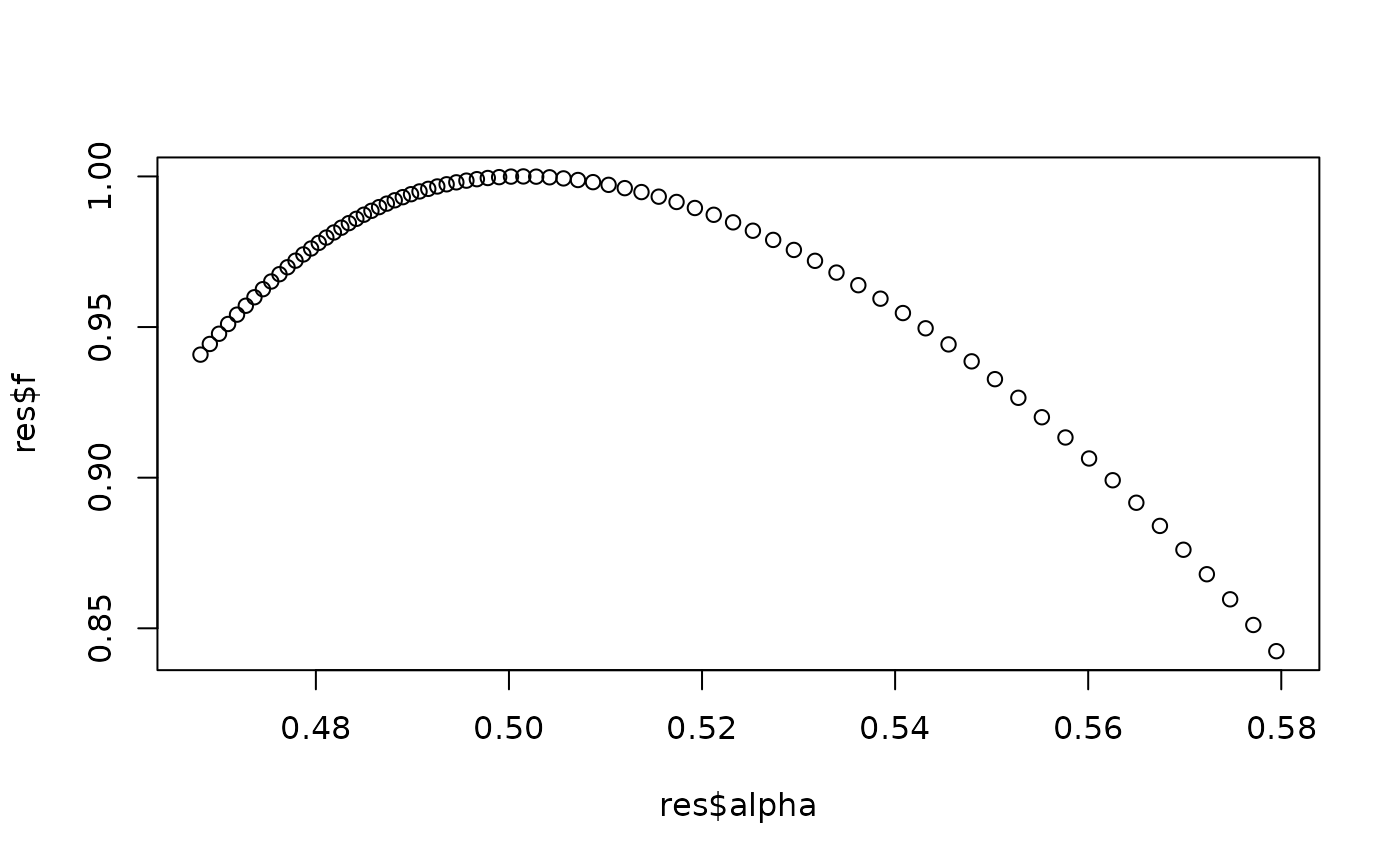

- alpha

Singularity strength alpha(q) (trimmed at both ends by the local-slope smoothing window; shorter than

q).- f

Multifractal spectrum f(alpha).

- q

The

qvalues corresponding toalpha/f(trimmed to match).